UK operators and taxpayers can save in the long run

Coupled with falling oil prices, decommissioning costs in the North Sea are coming up above the original budget. This puts operators with oil and gas platforms in the region, such as Shell whose Brent decommissioning project will take many years and accrue high costs, in a tight spot.

However experts remain confident that costs can come down, providing operators plan effectively, are open to alternative approaches to decommissioning and ensure there is clear cross-sector communication throughout the supply chain.

Where is the industry at?

Decommissioning of oil and gas projects in the North Sea is set to witness major growth in the long-term future. It is estimated that 478 platforms will need to be removed by 2045 and around £30 to £40 billion will be spent on decommissioning in the next thirty years in the UK alone.

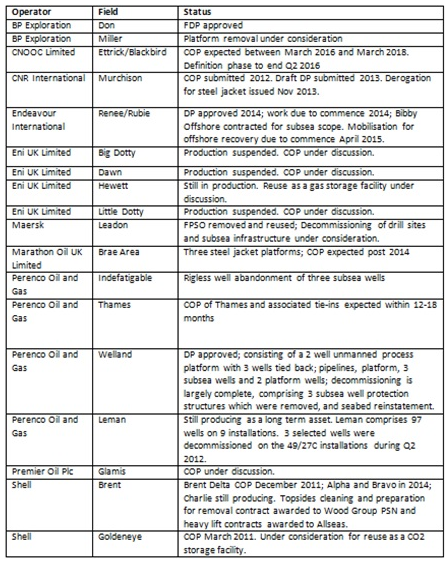

Table 1: Current decommissioning projects in the North Sea accroding to Project Pathfinder

Source: Adapted from the North Sea Decommissioning Report

FDP - Funding Decommissioing Program

DP - Decommissioing Program

According to the Department of Energy and Climate Change (DECC) there are more than twenty fields that are either currently undergoing or likely to undergo decommissioning in the near future. Significantly, of the projects listed in the table above, the majority of operators have more than one field. Whilst majors such as Shell and BP each have two fields in the decommissioning pipeline, independents are taking the lead, with Perenco Oil and Gas and ENI UK Limited having four fields respectively.

The decommissioning process represents a significant cost for operators and UK taxpayers alike, each of whom foot 50% of the overall bill. This is a particularly crucial consideration seeing that the purse strings are tight in light of the recent drop in oil prices.

Furthermore, as the offshore decommissioning process gains maturity, operators are getting a more realistic understanding of what the actual costs involved are, and in many cases this is far above the original budget.

However, experts remain confident that decommissioning costs can come down with effective planning, alternative approaches to decommissioning and cross-sector communication throughout the supply chain.

North Sea Decommissioning at a crucial turning point

Jonathan Turner, Senior Project Manager at ABB, argues that the North Sea decommissioning industry is at a crucial point. To date there have been around 25 platforms in the North Sea that have been decommissioned, almost all of which employed a single lift removal strategy making use of heavy lifters.

However, over the next couple of years more than 30 platforms will need to be decommissioned and removed and there are not enough heavy lifters available to undertake this work.

“Operators may end up having to wait around five years after Cessation of Production (COP) has been achieved before a heavy lifter becomes available”, Turner comments.

There are alternative methods such as piece small decommissioning which could offer a more immediate and cost-effective solution, but remain largely untested in the offshore decommissioning market, despite having a track record onshore.

“Operators are currently racing to be second”, says Turner. However, he remains optimistic that down the line operators will open their minds and pockets to new approaches. Piece small decommissioning, which involves sending workers aboard a platform to dismantle it piece by piece, can offer a 40% cost advantage over single lift removal, according to Turner.

“There is a window of opportunity between now and 2017. Every single job on a platform towards the end of life is piece small. Because equipment needs removal prior to COP, piece small activities are already underway”.

Whilst it remains unclear whether operators will adopt new approaches to avoid the inevitable bottleneck, what is clear is that delaying decommissioning after COP could end up harming their bottom lines.

Why delays will ultimatly cost operators

There have been some reports that operators are dragging their feet when it comes to initiating decommissioning procedures. Decommissioning requires cash and ploughing money into a field that is not producing may be a hard sell.

However, commencing decommissioning as soon as possible after the COP may be the lesser of two expensive undertakings.

“To maintain a platform that is not producing costs about £20 million per annum. The longer the window between COP and final removal the more it is going to cost the operator,” comments Turner.

After COP is achieved, operators still need to ensure that the platform is maintained for health, safety and environmental reasons. Furthermore, decommissioning a poorly maintained platform can lead to unforeseen risks, delays and costs.

Communication is key

When asked what the biggest risk facing the industry is, a common answer is the lack of communication between the late life team overseeing the COP and the decommissioning engineers.

“It is important that the guys who are handling the removals and the decommissioning teams talk to the end of life guys and tell them what they need in terms of what needs to remain live, what needs to be decontaminated and to what standard,” says Turner.

Failing to do this means that even a simple factor, like turning off a fire water pump after COP, can end up costing the operator millions during the decommissioning phase.

Sharing lessons learnt and planning ahead

It is estimated that costs may be reduced by 10-15% through incorporating the lessons learned from previous successive decommissioning projects.

According to Alan Stokes, Global Decommissioning Manager at Worley Parsons, “Projects that are going on at the moment are very interesting because they are effectively a second generation of decommissioning projects and have learnt a lot from the previous projects and are being carried out more effectively”.

The idea of creating a more co-operative communication channel is supported in the recent Wood Review and the 2014 Oil and Gas UK Decommissioning Insight. Both highlight the need for operators to not only co-operate with each other, but also to develop “a dedicated decommissioning strategy with effective early planning and coordination” not just for projects which have undergone COP, but for all future projects.

Whilst sharing lessons learnt and planning ahead may offer cost reduction benefits, the challenge will come in converting this from a ‘nice to have’ to an absolute industry requirement. “A lot of this is thinking 20 to 30 years ahead”, comments Stokes. In the immediate future, operators can benefit by adjusting their existing maintenance strategies to allow for a smoother, less costly decommissioning process, ensuring that delays after COP are avoided and, finally, making sure that alternative decommissioning strategies, such as piece small, are taken into consideration.